The New Power Brokers

The New Power Brokers

Plus: Spanish Bank Consolidation, More Ant Group, Independent Equity Research

Issue #16 of Net Interest, my newsletter on financial sector themes. Welcome to all those who’ve signed up since last week. We’re now over 5,000 subscribers, which is incredible! Every Friday I go deep on a topic of interest in the sector and highlight a few other trending themes. If you have any feedback, reply to the email or add to the comments. And if you like what you’re reading, please do share and invite friends and colleagues to sign up.

The New Power Brokers

Around ten years ago a new book came out about Goldman Sachs, called Money and Power: How Goldman Sachs Came to Rule the World. It’s a gripping book—the tale of Goldman’s rise from immigrant founded startup to global behemoth. The problem is, its title is outdated. While it may have been true ten years ago, it’s no longer the case that Goldman Sachs rules the world.

Since the financial crisis, the influence wielded by Goldman and banks like it has slowly eroded. In their place are the Big Tech companies, of course [1]. But within financial markets specifically, power has shifted to another group of companies. It’s a group whose origins predate the big banks and who lost a power struggle to them only a few years before the crisis. That group is the stock exchanges.

Over the past few weeks Net Interest has discussed the exchanges from various angles:

In mid-August, we did a detailed write-up on ICE, the biggest exchange group in the world.

Then we took a look at Bloomberg, which channels exchange data but also offers its own trading platform and owns an index provider.

Last week we wrote a guest post looking at the New York Stock Exchange’s quest for monopoly.

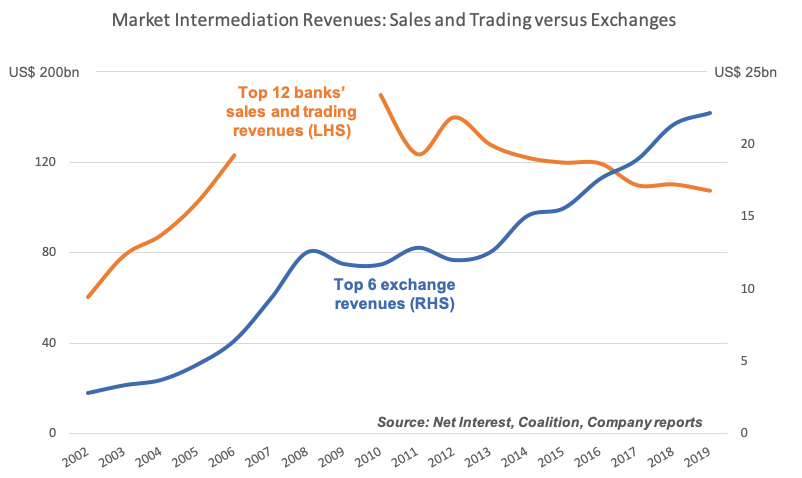

This week we zoom out to take in the whole exchange industry. Once a collection of low agency marketplaces, exchanges now control most of the infrastructure that enables the functioning of capital markets. They continue to provide a venue for securities trading, but in addition they offer a broad range of financial products, indices, data and post-trading services. By combining these activities and consolidating their markets, exchanges have dislodged the big banks from their position as rulers of the world.

How they got here

Many years ago exchanges were mutually owned by their customers. In the days when customers consisted mostly of small brokerage partnerships, the power dynamic held. But as soon as customers began to consolidate into the big banks they are today, a power shift took place. Coinciding with cheaper technology, the big banks wanted to go alone. They set up alternative trading venues and established new exchanges. Today, there are around 50 alternative trading venues in the US and 13 exchanges.

One by one, exchanges around the world were sold off by their former owner customers. The first to demutualise was Stockholm back in 1993. By the end of 2000 there had been a rash more, including London, the Chicago Mercantile Exchange (CME) and NASDAQ. Today, not one of the world’s major exchanges is anymore structured as a mutual, and nearly three quarters are publicly traded.

Infused with a profit motive just at the time their industry was (a) fragmenting, because of big bank new entrants and (b) globalising, exchanges embarked on a massive merger and acquisition (M&A) wave. Deals were forged to build scale across both cash equities and derivatives markets. Deals like the NYSE merger with Euronext in 2007 and NASDAQ’s acquisition of the Stockholm and other Nordic exchanges in 2008. A number of high profile merger attempts also failed, such as ICE for CBOT and the London Stock Exchange for Toronto.

In most cases the logic was to eliminate costs (in a typical merger 25-40% of target costs could be taken out) and reclaim the edge in scale that can have disproportionate benefits in a network-driven business. Twelve of the 13 exchanges in the US are now owned by three firms.

[Source]

This first round of M&A was largely defensive. After the financial crisis, exchanges embarked on a new round of M&A that was much more offensive. Faced with declining margins in their traditional trade execution businesses, exchanges moved into adjacent markets. They began scooping up assets in market data and indexing and fixed income electronic trading.

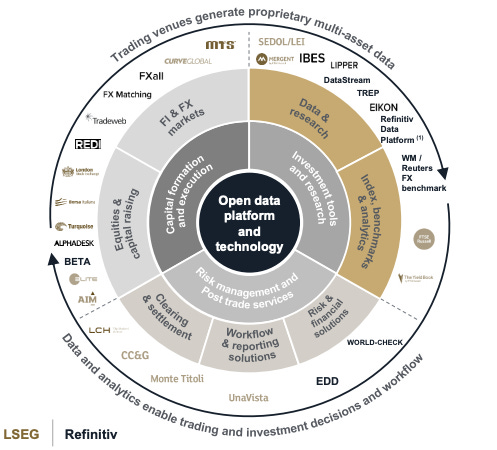

The very biggest of these is currently in the works. Last year the London Stock Exchange bid US$27 billion to acquire Refinitiv, the second largest market data company globally, behind Bloomberg. The deal is still pending regulatory approval but when it goes through it will transform the London Stock Exchange into a leading global financial market infrastructure provider. As a combined group, the company touches multiple markets:

The most important thing about these complimentary markets is that they are more consolidated than trade execution. Trade execution fragmented with the entry of those 50 alternative trading venues into the market. The New York Stock Exchange, for example, lost half its market share. In contrast, just four players control around two-thirds of the industry for market data and among index providers, three players have around 80% of the market.

As someone clever on Twitter said:

So while they were shoring up their position in complementary markets, exchanges were complicit in commoditizing their legacy trade execution businesses. Jeff Sprecher, the CEO of ICE, which owns the New York Stock Exchange, said (emphasis mine):

“I believe that execution is not particularly valuable… I think over time finding a buyer and a seller in a world where we have the Internet is really the most simple thing in the world, and networks can form up overnight to find buyers and sellers… And it was helpful to buy the New York Stock Exchange, because I think the New York Stock Exchange essentially is at zero. We don't run it that way because it's a whole big business. We don't break out execution, but I don't think there's any money – I mean, we may lose money on execution if we were to really allocate cost. And how do we make the money? Data, listings, connectivity, information, catering, we print banners, I mean, everything around the execution is where we make money. And so that helped inform us that execution is probably in a digital world is going to go to zero.”

I don’t know how much money the New York Stock Exchange makes in catering or printing banners, but the other areas are certainly lucrative! More than that, these areas – together with the clearing businesses which sit in ICE – are the source of the exchanges’ newfound power.

Sources of power

Following the financial crisis, two key developments helped to shift the centre of gravity in financial markets from the big banks towards the exchanges.

The first was regulation. In the aftermath of the crisis, regulators looked to bear down on big banks. In particular, they wanted to introduce tighter regulation around derivatives. Tension between the New York-based dealers (the big banks) and the Chicago-based exchanges had long been a feature in the evolution of derivatives regulation. Prior to the crisis the dealers usually won out, being allowed to trade derivatives between themselves in an over-the-counter market. After the crisis, however, new regulations were enacted mandating that all sufficiently standardised derivatives should be cleared into a clearinghouse.

And who owned the clearing houses? The exchanges. While in 2006 exchanges owned 55% of central counterparty clearing houses globally, by 2014 that proportion was up to 83%. Today, following further acquisitions made by the London Stock Exchange and CBOE, the proportion is even higher.

Owning a clearing house confers considerable power when it comes to financial markets. Clearing houses decide on the collateral and capital requirements counterparties need to post when they trade. They decide which assets are safe enough to back transactions and which are not.

This power was exercised at the expense of the Italian Republic at the height of the Eurozone sovereign debt crisis. In November 2011, clearing houses raised their requirements against positions in Italian government securities “based partly on discretionary criteria” (according to a report by The Banca d’Italia). The substantial increase in margins had a big impact on the secondary market of Italian government bonds, provoking a widening of their spread against safer German bonds and causing “liquidity strains for participants in the guarantee system” (the Banca d’Italia again).

Not four years earlier it was the big banks issuing margin calls. The book about Goldman Sachs tells of a collateral call Goldman placed on AIG at the beginning of AIG’s slide to ignominy. “Sorry to bother you on vacation,” wrote a senior managing director at the firm to his counterpart at AIG. “Margin call coming your way. Want to give you a heads up.”

The license to disturb vacations has transferred to the clearing houses—and they don’t say sorry.

The second key development that has helped exchanges climb the power ladder has been indexation. One of the key features of public equity markets over the recent past has been the growth in assets strapped to some benchmark index at the expense of assets managed on an active basis. Since 2008, investors have directed US$2.0 trillion into index mutual funds and exchange-traded funds and more than US$1.8 trillion out of active funds.

The headline winners of this trend have been those asset managers that dominate passive management—firms such as Blackrock and Vanguard. However, pulling the strings behind the scenes are the index providers. Blackrock and Vanguard may look after the money, but they delegate investment decisions to index providers.

And with the exception of MSCI and Bloomberg, all large index providers are owned by stock exchanges: FTSE and Russell are owned by the London Stock Exchange, S&P and Dow Jones are partially owned by the Chicago Mercantile Exchange, Stoxx is owned by Deutsche Börse and NASDAQ is owned by … NASDAQ.

Once the purview of financial media enterprises, equity indices have migrated into the hands of exchanges at a time when they are becoming more entrenched in the system. No longer do they simply supply information, they now exert authority.

This was on full show this week when the Dow Jones Industrial Average kicked out ExxonMobil from among its constituents and added Salesforce. The Salesforce stock price jumped 4% on the news (which is more than a Goldman upgrade would have prompted). Similarly, two large European banks are being kicked out of the Euro Stoxx 50 index later this month, forcing some of their largest shareholders to sell. It’s not just size (or in the case of the Dow, stock price) which determines these changes—index providers frequently look at corporate governance metrics as well. In this way, they exert influence over how a company behaves along such dimensions as shareholder structure, voting rights and even domicile. The launch of ESG indices is an extension of that.

Whole countries can be affected, too, like when MSCI decided to include China A-Shares into its MSCI Emerging Market indices. The process involved much political wrangling, with MSCI eventually forcing concessions out of China that other power players couldn’t.

And it’s not just equity. Although fixed income markets have historically been influenced more by credit rating agencies, the growth of exchange traded funds in fixed income is giving index providers a greater role. Over the past few years exchanges like ICE have acquired fixed income indices from the big banks that devised them.

It’s pretty well established that the Fed – indisputably one of the most powerful institutions on Earth – is driving markets right now through its expansionary policy. What’s less well established is that the index providers are steering them. The FT’s Robin Wigglesworth was not exaggerating when he wrote, “Financial indices are arguably the most under-appreciated force shaping global markets.”

The New Power Brokers

Linked to regulation and indexation are a number of other developments that combine to skew power away from the big banks and towards exchanges. The New York Stock Exchange recently announced that it is going to allow companies to raise capital via direct listings. This neuters some of the power that banks retain through their control of the IPO process.

Banks have also lost their ability to set the key interest rate benchmark, LIBOR. Unlike the other factors listed, this one was entirely of their own making. Markets now have until the end of 2021 to migrate US$350 trillion of assets over to a new benchmark—a market-driven benchmark (tradeable on CME) not decided by a panel of big banks.

Whether it’s via clearing, indices or the products they offer, exchanges are increasingly assuming the authority to create the rules which underpin market transactions. By shaping the rules of the game, exchanges exercise structural power over the companies, investors and states who utilise their infrastructures.

The power would not be so potent if it were not so concentrated. Six global stock exchange groups control 62% of the revenues in the space. Even though big banks have consolidated from the days when they were small partnerships, it takes over ten of them to get to that degree of concentration.

The book about Goldman cites an Economist leader from 2006, titled On Top of The World: “Goldman Sachs is a formidable company… Even compared with leaders in other industries, Goldman makes spectacular returns.” Today it is the exchanges which generate spectacular returns. CME and ICE have two of the highest pre-tax profit margins in the S&P 500. Last week the Economist honed in on them, under the title Big Fish.

The power shift is complete.

Thanks to Johannes Petry whose excellent paper provided the foundation for this piece.

[1] In 2009 Goldman Sachs was famously described as “a great vampire squid wrapped around the face of humanity, relentlessly jamming its blood funnel into anything that smells like money.” In 2018 the description was turned on Facebook by British lawmakers at a parliamentary hearing.

More Net Interest

Spanish Bank Consolidation

Further European bank sector consolidation has long been inevitable. There are simply too many banks on the continent, operating too many branches. Revenues are under pressure from low interest rates and Covid has exacerbated that. Meanwhile branches are underemployed and Covid has exacerbated that. So it makes sense that two Spanish banks are getting together. Last night CaixaBank, the largest domestic bank in Spain by loans, confirmed that it is in talks to merge with Bankia, the fourth largest.

Spain has more bank branches per capita than any other major country in the Eurozone, so the cost savings opportunity should be high. Because both banks trade at a discount to their net asset value, capital will be released in the transaction. This capital (known as badwill because it’s the technical opposite of goodwill, even though there’s nothing bad about it) can be used to absorb up-front restructuring costs. Without it, it would be difficult to absorb restructuring charges and maintain regulatory capital levels.

The deal suggests some confidence in the current environment. The banks’ combined share of Spanish lending is close to 30% so they should have a fairly good handle of what’s going on. It may pave the way for mergers in other European countries, but for now they are likely to be domestic. Before cross-border mergers happen in Europe, policymakers need to make more progress on banking union.

More Ant Group

We did a detailed write-up of Ant Financial here a few weeks ago and provided an update following publication of its IPO prospectus last week. One key question is whether the company can sustain growth in its ‘CreditTech’ business if credit conditions begin to deteriorate. The concern here is that the banks which Ant passes loans onto could get skittish in a downturn.

How real a risk that is depends on Ant’s ability to select the best credit. Credit performance has so far been better than the overall system. An interesting paper published by the BIS this week highlights the differences between the data-based credit assessment employed by Ant and more traditional bank credit assessment. It confirms that Ant is much less concerned with collateral values underpinning loans or local economic conditions than traditional banks. If it has indeed found a magic sauce then not only will that sustain its credit business for longer, it has implications for the future of economic policy. According to the BIS, “This evidence implies that a greater use of big tech credit – granted on the basis of machine learning and big data – could reduce the importance of collateral in credit markets and potentially weaken the financial accelerator mechanism.”

Independent Equity Research

A few weeks ago I wrote a popular post on equity research. Last week the European Association of Independent Research Providers released results of a survey they conducted among their members. They confirm deflation in the market for equity research. Three quarters of independent research providers see research prices as either flat or declining further in the next two years. They blame pressure from the big investment banks: two thirds argue for regulatory action on predatory and unfair competition. I guess free Substacks aren’t helping either?

Love these historical pieces, very eye opening

hi Marc, how does the provider of the index financially benefit? For example, S&P500 is an index which SPY tracks which in turn people invest in. How does value accrue to the index provider in this instance? thanks.